This week in crypto. Jan 24-30: Crypto investors vs the old finance, social networks embracing NFTs and more...

An equal society where all people have the chance to succeed is one of the major preoccupations of the century, but the world is struggling in making it come true.

Some might argue that (more) money should be taken from the rich and given to the poor, but we think that this would only bring up some serious moral debates, and also be totally counterproductive. We believe that the best way to equal possibilities for all starts with the system that fuels our economies and governs our lives to the extent we might not even fully comprehend – the finance 💰

Tight circle of the old finance

Big finance is naturally tied to the money creation. Through the magic of Quantitative Easing Central Bank creates money, with which it buys bonds from the state and corporations. Which ones? Central Bank decides.

The Central Bank can also create and lend money to the commercial banks, which then have a possibility to buy products and assets whose prices have not yet risen due to the increase in the money supply.

As a rule, people and institutions with the closest ties to the Central Bank are given financial advantages at the expense of those with the fewest links to the financial system.

Traditional financial system is built by and led by a tight circle of bankers, government officials and other finance specialists. It is very complex, and financial products containing derivatives of derivatives of derivatives… of an asset are all too common. Financial market regulations aren’t much easier, and it often takes an army of lawyers and accountants to make sense of it.

It’s not surprising that financial instruments are mostly reserved to specialists, and even the simplest products like stocks often cannot be directly bought by an average person. Services like Robinhood started challenging this by allowing people bypass their bankers and trade stocks themselves – and they have become a great success, attracting millennials in search of financial independence.

Crypto investors

Crypto and Web3 have pushed the limits of accessibility much further, changing many things about investments. A young industry with a remarkable potential that can be joined by anyone, anywhere, without red tape, authorizations, licenses… No discrimination, no glass ceiling. Only requirement: DYOR (do your own research).

The nature of the assets is much more obvious too. While banks amused with incongruous financial products like, among other monstrosities, CDO Squared (collateralized debt obligations backed by another collateralized debt obligations backed by credit default swaps 🤯), crypto has a very clear value proposition.

Independent and borderless money. Currency allowing to deploy and run programs on a decentralized network. Picture of an Ape giving access to the community of creative people. Character in a video game.

Crypto investors, especially early ones, were people believing in technology and community, and not believing in banks. Their number increases every day, and their demographics is totally different from the financial world.

NORC, a research body within the University of Chicago, looked into the American crypto investors demography this summer and found that the average crypto trader is under 40 and does not have a college degree (55%). 44% of crypto traders are not white, and 41% percent are women. 35% have household incomes under $60k annually.

Such demographics would be a dream of any equality committee, and it shows how crypto is opening investing opportunities for more diverse investors. And yet, there are people who find it disturbing.

Stupid little people

Paul Krugman is a Nobel-prize winning economist and a regular columnist for The New York Times. He is famous for his 1998’s prediction of the death of the Internet and his 2013’s post titled “Bitcoin is Evil”.

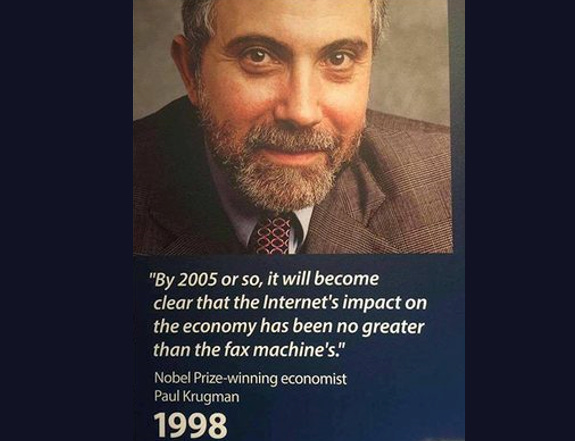

In his latest piece he took notice of the NORC research, but made very different conclusions. Paul Krugman compared crypto investors to the people who were given mortgage loans that exceeded their financial possibilities, and who were the first victims of the 2008 subprime crisis. He failed to mention the role of banks, which packaged bad debts into ever more complex financial vehicles, and rating agencies, which gave the best notes to their brothers in arms, green-lighting the whole world that these financial products were sound, and making the crisis global.

The conclusion that Paul Krugman arrived at after this peculiar comparison was that crypto investors "should be people who are both well equipped to make that judgment and financially secure enough to bear the losses if it turns out that the skeptics are right". He made clear that the current crypto investors demographic witnesses to the contrary, i.e. the fact that crypto investors being not all rich white men is worrisome. Wall Street giants investing billions of dollars in crypto are ok: they wear suits.

The fact that Krugman himself, being a rich white man with a college degree and even a Nobel prize, has notoriously missed trillions of dollars of value created on the Internet, and then - Bitcoin and other crypto, does not bother him a bit. Nor does the fact that, despite being volatile, Bitcoin price has only went up, and the Americans who bought Bitcoin with their Covid stimulus check in March 2020 have made a 543% gain (over 1000% gain for those who managed to cash in at Bitcoin’s highest last November).

Stupid little countries

Countries can also be patronized, by bigger ones or international organizations. IMF bullying El Salvador into abandoning Bitcoin as legal tender took the same condescending tone in warning about “financial stability, financial integrity, and consumer protection”.

Is IMF genuinly worried about the financial stability of Salvadoran households, or it is trying to protect the current dollar-based financial system, is another question.

Teach a man to fish

Paul Krugman and many politicians around the world brandish the “consumer protection” banner in a condescending attempt to protect people from themselves and keep them within their roles of cogs in the well-oiled machine of the global finance. The increasingly interventionist governments are happy to comply: giving people some seemingly free money is an easy way to earn popular support.

We believe that instead of being infantilized, people should be empowered, and what a better way to do this than with crypto.

Crypto allows anyone to acces the world of finance. Be it the US Black and Latino communities locked out of finance, unbanked Salvadorans, or people in any part of the world keeping their savings in a 1%-yield bank account. Can these people loose money, investing in crypto? Of course they can. They can also gain some. That’s how investments work.

Instead of denying access to crypto, a good-intentioned politician would rather concentrate their efforts on education, promoting good knowledge about the blockchain, cryptocurrencies, online security and the basics of supply-demand equilibrium, which determines the price.

However, most of them do their best to keep the status quo, perhaps because the current system is effective in fighting inequality and making people’s lives better.

Oh wait, it is not.

NFT and Metaverse

NFTs are on their way to becoming an important part of people’s social identities: they indicate belonging to a community, caring about a goal… in other ways, they help people express themselves online. Just like their social media activity.

It’s no surprise then that social networks turn their eyes to NFTs and notably the possibility to integrate a special feature showing that a user possesses the NFT on their avatar.

Twitter (436M users) was the first to launch it on January, 20 (although only in the US, and only for the Twitter Blue subscription service - at least for now). A couple of days before this Meta announced it was working on allowing Instagram (1.4Bn users) and Facebook (2.9Bn users) users displaying NFTs as profile pictures. This week it was Reddit (430M users) who said they were testing the same feature.

Together these social medias have billions of users and can take the NFT hype to the next level by leveraging the network effect. It looks like NFTs are here to stay.

Markets

Bitcoin

Bitcoin price hit its lowest level since July - $33k, before gaining +12%, which put it above $37k.

It was a welcome bounce, especially taking into account the intensifying threat from the US regulators: the White House is said to be preparing an executive order on crypto (and there are little chances it will be friendly), while the Senators will be discussing the America COMPETES Act of 2022, which contains provisions giving the Treasury unchecked powers to ban any financial asset, including crypto.

Good news this week came from Russia, where the Head of Central Bank, a notorious crypto hater who proposed to ban crypto, was confronted by President Putin and told to “not stand in the way of technical progress”.

Ethereum

Ethereum price plunged as low as $2’170 on Monday, but has regained 17% since.

Quote of the week

“The government does not need to make financial decisions for the American people. Our $30 trillion national debt should be your first hint at that.”

Cynthia Lummis, US Senator for Wyoming, on the America COMPETES Act 2022